Macroeconomic Outlook

REPORT

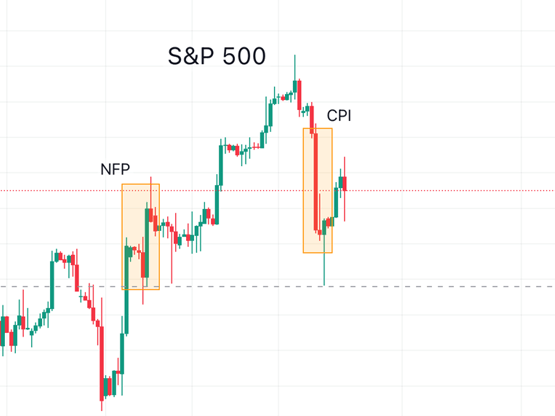

In the last few days, we have seen the release of very important data for the United States, such as the NFP (non-farm payroll) and the CPI (consumer price index).

Both data have been higher than expected, which leads us to think only one thing: we will not see a rate cut by the FED (Federal Reserve System) in March.

The employment data [currently 353k] reflects that even with relatively high rates, there is not a problem in the employment sector (at least on the surface; something to consider is that people in the United States may be working but may now require more than one job to earn the same as before), therefore a rate cut announced in March would not be necessary.

The same goes for the CPI [actual 3.1%, expected 2.9%]. Being higher than expected means that inflation is still "high" and a rate cut would not be necessary.

How have the markets reacted to the news?

The American indices have been resilient to the employment data and previously to the GDP data, setting new historical highs in the last few days (S&P500 at 5000 points). On the other hand, the inflation data has reflected falls of between 1 and 2% in the different indices. The expectation that interest rates will not fall means indirectly that companies will have to finance themselves even at current rates, which would mean paying more for financing.

Here is how the market reacted:

Is this worrying?

Not at all. The rally in the indices is historic, and a small correction would even be healthy to continue the upward trend. All this always bears in mind that a recession would be possible by 2025, and this could destabilize the market.

On the other hand, as the US is in an election year, recurring attempts will be made to politicize economic decisions, and we will see increasing accusations from politicians: "The Republican Party is already saying that cutting rates this year is just a way to give the Democrats a boost by helping the economy before the election." Democratic lawmakers, including Senators Sherrod Brown and Elizabeth Warren, sent letters last week urging Powell to lower interest rates. And former President Donald Trump told Fox Business Network on Friday that he "wouldn't reappoint Powell," an important statement considering he chose him to lead the central bank in 2017.

To sum up, few now doubt that in 2024 there will be a change of course in monetary policy; the big question is when and how much. Here is where investors and speculators play.

Conclusion: